While they have us freaking out about “Ukraine,” our overlords are moving swiftly to

rendition all of us into the global cyber-gulag of a social credit system, enabled by a digital currency doled out (or not) by the central banking system.

(Article by Mark Crispin Miller republished from

MarkCrispinMiller.Substack.com)

This report, from December, 2021, “assess[es] market opportunities for infrastructure support of the social credit market”—i.e., how to make a lot of money helping to set up that cyber-prison. Unless you’re reading it for “market opportunities,” you’re likely to be chilled by its dystopian implications.

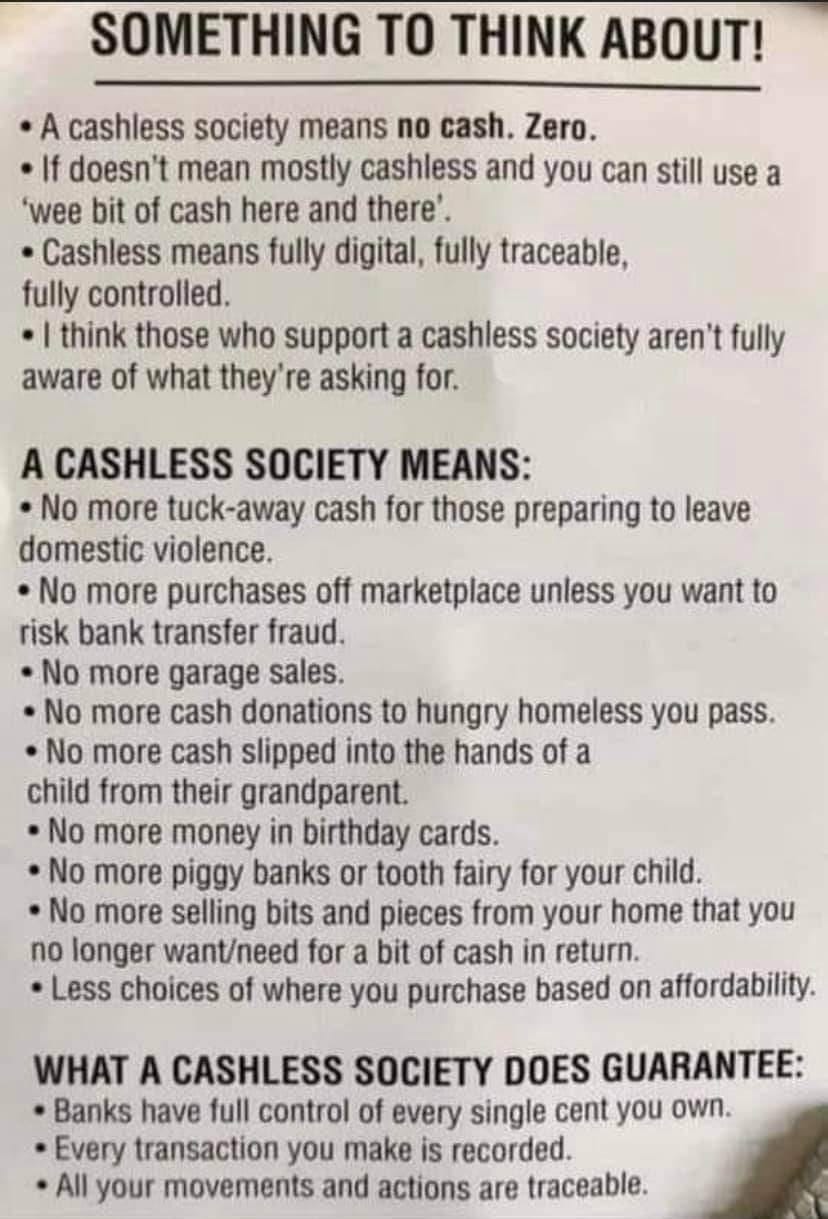

One way to start fighting this development is to go back to using

cash instead of cards as much as possible—starting with #CashFriday, as urged by Catherine Austin Fitts. This means that, every Friday, we use

only cash to buy what we may need: https://home.solari.com/cash-friday/.

Think about what this development portends: No cash will mean

no autonomy, as every purchase that you’ll want to make must be approved on high—approval that will be contingent on your social credit score.

She’s absolutely right about what’s happening: https://www.instagram.com/reel/Ca55xTwlr6H/?utm_medium=copy_link

James Corbett on the looming social-credit prison: https://www.bitchute.com/video/3Tl5G0BPua7q/

Here’s a summary of the report on “market opportunities” in setting up the “infrastructure” for the new panopticon. (The whole document costs $2,500 for single readers.)

Social Credit Market by Physical and Cyber Infrastructure (Sensors, Cameras, Biometrics, Computer Vision), Software (Machine Learning, Data Analytics, APIs), Use Cases, Applications, Industry Verticals, and Regions 2021 – 2026

- ID: 5134311

- Report

- December 2021

- 121 Pages

https://www.researchandmarkets.com/reports/5134311/socialcredit-market-by-physical-and-cyber

This is the only report of its type to assess market opportunities for infrastructure support of the social credit market. The report evaluates market drivers, use cases, and consequential impacts/implications (anticipated and likely unanticipated) for social credit market implementation and operation.

The report also evaluates some of the leading companies that are anticipated to drive social credit market evolution. This report includes detailed quantitative analysis driven by market needs with forecasting for all major infrastructure elements from 2021 to 2026.

Select Report Findings:

- The COVID-19 pandemic has facilitated substantial interest in citizen monitoring solutions

- Infrastructure to support social credit systems represents a $16.1B global opportunity by 2026

- Cameras and other optical equipment for social credit systems will reach $723M globally by 2026

- Advanced computing will be used in conjunction with AI to provide nearly flawless identification and tracking

- Various forms of biometrics will be used for identity verification as well as verifying the presence/location of people

- Starting as tangential to public safety and homeland security, the social credit market becomes mainstream by2026

- Social credit systems represent the ability to identify (mostly people but also some “things”) and track activities for purposes of grading behaviors and applying “social credit” scoring. A given grading/scoring methodology depends largely on social credit system objectives and metrics.

However, most systems will have socially acceptable behaviour at their core. This presents both a challenge and an opportunity as a combination of government, companies, and society as a whole must determine “good”, “bad”, and “marginal” behavior within the social credit market.

Beginning as a trend largely orthogonal to public safety and homeland security concerns, the market for social credit system infrastructure will ultimately become a mainstream component of both business and public policy.

This means that systems will ultimately be used for a variety of commerce and lifestyle-related issues ranging from risk assessment (access to credit, financing fees, insurance, etc.) to accessibility within public places such as concerts, sporting events, and other assemblies. High social scoring individuals within the social credit market will be granted preferred access to both real and digital assets.

Social credit system infrastructure includes analogue and digital surveillance, Internet-enabled devices like smartphones, wearable devices, security systems, sensor-enabled physical objects, and surveillance devices that use biometrics and computer vision. Technologies include broadband wireless (WiFi, LTE, and 5G), IoT, AI algorithms, and big data analytics platforms, processes, and procedures.

While each of these systems has market value individually, and are deployed separately for various purposes, it is the convergence of these otherwise disparate technologies that will facilitate value within the social credit market. For example, combined AI and IoT systems will be leveraged to identify important events that require immediate action versus those that are merely archived.

It is important to note that there is great overlap between the technologies used for social credit systems and other solutions such as public safety, homeland security, and smart cities applications of many types including smart transportation (highways and surface streets, parking, autonomous vehicles, etc.), intelligent buildings, environmental monitoring (light, temperature, pressure, etc.). Many of these infrastructure elements are already planned for smart city implementations and will, therefore, be multi-purposed including support of the social credit market.

In terms of physical infrastructure, social credit systems will rely upon various forms of equipment and platforms including sensors, biometrics, cameras, and other optical devices, computer vision systems, and other advanced computing platforms.

Cyberinfrastructure includes platforms, devices, and software to support data processing and correlation with identity information, which shall leverage AI, IoT, and advanced data analytics. The main purpose for all the aforementioned infrastructure elements is to capture data, which must be stored and acted upon as appropriate.

At the heart of social credit, systems are large-scale data repositories that may store virtually any type of data that may be correlated to or associated with citizens and businesses in terms of both identity and behaviors.

This includes raw observational data as well as listings (white, grey, red, and black) and meta-data to tie together data elements and allow for ease of information queries. Without the use of AI and big data technology, it would be problematic to implement social credit market systems in a meaningful way as massive amounts of disparate data must be correlated.

With the purchase of this report at the

Multi-user License or greater level, you will have access to

one hour with an

expert analyst who will help you link key findings in the report to the business issues you're addressing. This will need to be used within three months of purchase.

This report also includes a

complimentary Excel file with data from the report for purchasers at the

Site License or greater level.

Read more at:

MarkCrispinMiller.Substack.com