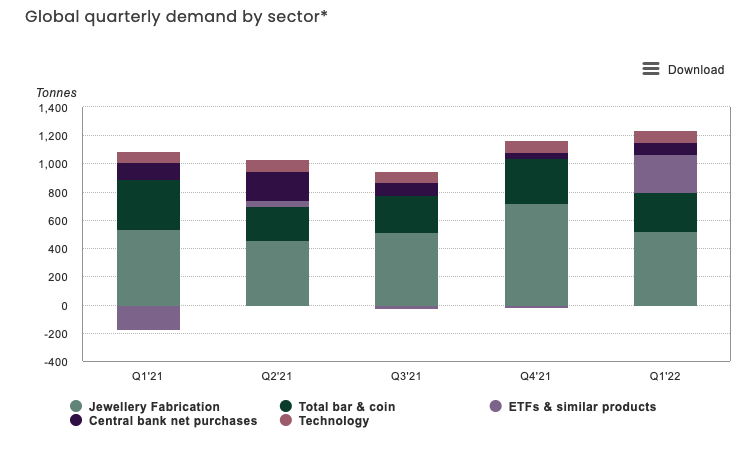

Gold inflows into ETFs charted their strongest quarterly number since the third quarter of 2020. Safe-haven demand fueled the 269-ton increase in ETF gold holdings. This more than reversed the 174-ton outflow from gold-backed funds in 2021.

Demand for gold coins and gold bars came in at 282 tons. That was 20% down from a very strong first quarter last year, but it was still 11% higher than the five-year quarterly average.

While physical investment gold demand in the US and Europe were both strong, China was key to explaining the y-o-y decline. A drop in Chinese demand for gold bars and coins due to new government COVID-19 lockdowns put a drag on physical gold investment in that country. Record gold prices in some currencies also resulted in profit-taking. This was particularly true in Japan and Turkey.

Softer demand in China and India also stalled the recovery in the gold jewelry market. Q1 demand was down 7% year-on-year, coming in at 474 tons.

Central banks added a modest amount of gold to their holdings in Q1. On net, central banks globally increased their gold reserves by 84 tons. This doubled the increase from Q4 but was 29% down from the first quarter of 2020. Several central banks made large sales in Q1, pulling the net increase lower.

Demand for gold by industry rose by 1% year on year. It was the best Q1 for industrial gold demand since 2018.

While the technology sector has recovered somewhat from the impact of the pandemic, COVID-related headwinds remain thanks to China’s draconian policies. Dozens of cities in China are under total or partial lockdown, with major industrial and financial hubs such as Shanghai impacted. China’s zero-COVID policy also coincided with the Chinese New Year holiday. According to the WGC, this will potentially impact the electronics supply chain throughout 2022. The war in Ukraine could also impact the global electronics market moving into the second quarter.

Looking ahead, the WGC says that with so many factors in play, it’s difficult to determine gold demand trends moving forward.

Jewelry and industrial demand could see deteriorating market conditions if the war in Ukraine continues. But we could also see quickly improving conditions with a resolution of that conflict. It’s also hard to predict how governments will respond to any resurgence in COVID-19. More lockdowns would put additional drag on these sectors.

On the other hand, the World Gold Council says it expects investment demand to be higher this year than last year due to high inflation and geopolitical instability.

You can read the entire World Gold Council report HERE.

Read more at: SchiffGold.com

Gold inflows into ETFs charted their strongest quarterly number since the third quarter of 2020. Safe-haven demand fueled the 269-ton increase in ETF gold holdings. This more than reversed the 174-ton outflow from gold-backed funds in 2021.

Demand for gold coins and gold bars came in at 282 tons. That was 20% down from a very strong first quarter last year, but it was still 11% higher than the five-year quarterly average.

While physical investment gold demand in the US and Europe were both strong, China was key to explaining the y-o-y decline. A drop in Chinese demand for gold bars and coins due to new government COVID-19 lockdowns put a drag on physical gold investment in that country. Record gold prices in some currencies also resulted in profit-taking. This was particularly true in Japan and Turkey.

Softer demand in China and India also stalled the recovery in the gold jewelry market. Q1 demand was down 7% year-on-year, coming in at 474 tons.

Central banks added a modest amount of gold to their holdings in Q1. On net, central banks globally increased their gold reserves by 84 tons. This doubled the increase from Q4 but was 29% down from the first quarter of 2020. Several central banks made large sales in Q1, pulling the net increase lower.

Demand for gold by industry rose by 1% year on year. It was the best Q1 for industrial gold demand since 2018.

While the technology sector has recovered somewhat from the impact of the pandemic, COVID-related headwinds remain thanks to China’s draconian policies. Dozens of cities in China are under total or partial lockdown, with major industrial and financial hubs such as Shanghai impacted. China’s zero-COVID policy also coincided with the Chinese New Year holiday. According to the WGC, this will potentially impact the electronics supply chain throughout 2022. The war in Ukraine could also impact the global electronics market moving into the second quarter.

Looking ahead, the WGC says that with so many factors in play, it’s difficult to determine gold demand trends moving forward.

Jewelry and industrial demand could see deteriorating market conditions if the war in Ukraine continues. But we could also see quickly improving conditions with a resolution of that conflict. It’s also hard to predict how governments will respond to any resurgence in COVID-19. More lockdowns would put additional drag on these sectors.

On the other hand, the World Gold Council says it expects investment demand to be higher this year than last year due to high inflation and geopolitical instability.

You can read the entire World Gold Council report HERE.

Read more at: SchiffGold.com

By Lance D Johnson // Share

Americans relying more and more on DOLLAR STORES as inflation worsens

By Ramon Tomey // Share

War on Cash: Israel strictly regulates cash payments to curb “financial crimes”

By Belle Carter // Share

SEC ignores Paul Pelosi but charges 11 in alleged $300 million crypto Ponzi scheme

By JD Heyes // Share

UK High Court rules against giving control of $1 billion in gold reserves to Venezuela’s Maduro

By Arsenio Toledo // Share

The Real Reason You're Seeing 'Turbo Aging' Everywhere... and What It Means for Humanity

By healthranger // Share

If You Want to Live, Stop Trusting the FDA, CDC, Corporate Media, and Jab-Pushing Doctors

By healthranger // Share

The Assault on Vaccine Science: A review of the evidence for vaccine safety reform

By bellecarter // Share

Report: Iran, Oman Near Deal to Reopen Strait of Hormuz With "Service Fee" Collection

By garrisonvance // Share

Report: Pentagon Seeks "Creative" and "Unconventional" Ways to Pressure Iran

By garrisonvance // Share

White House Moves to Accelerate AI Data Center Development on Federal Lands

By edisonreed // Share